Dechert is one of the leading voices and thought leaders on the securitization and structured finance industry’s response to the risk retention rules of Dodd-Frank and the European Union. We’ve helped trade organizations and clients craft comment letters to the regulatory agencies and serve on key industry committees. As risk retention looms (it already applies to securitizations marked into Europe), we are actively developing structures and strategies for our clients to comply with this new and very consequential regulatory regime.

Dechert is one of four law firms working together to offer insight into key questions raised by the requirements of risk retention, commonly referred to as the Final Rule.

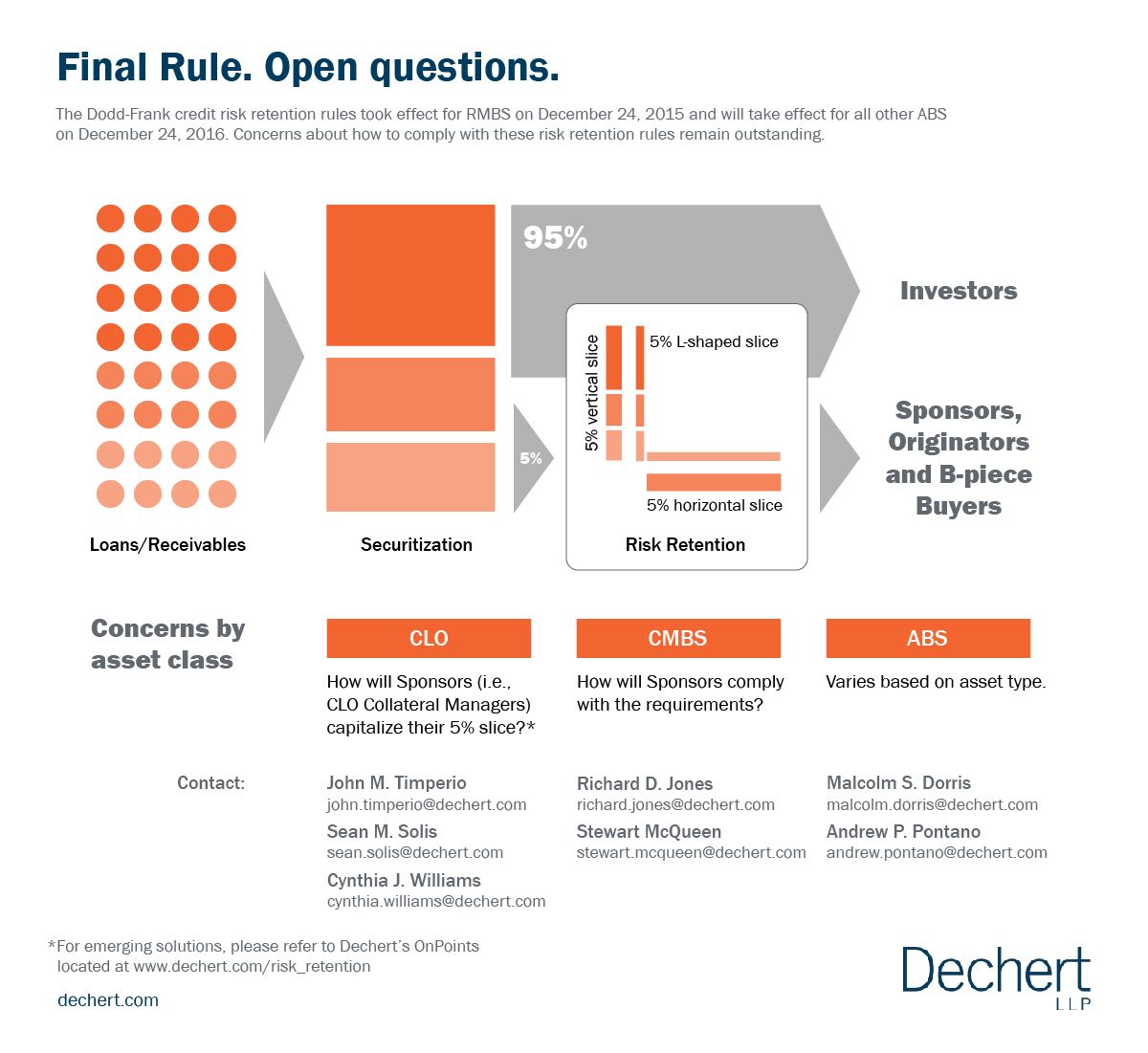

What is risk retention?

In late 2014, the Securities and Exchange Commission, the Board of Governors of the Federal Reserve System, the Department of Housing and Urban Development, the Federal Housing Finance Agency, the Federal Depositors Insurance Corporation and the Office of the Comptroller of the Currency promulgated final U.S. risk retention rules (the “Final Rule”) for asset-backed securities to implement the risk retention requirements of Section 941 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, codified as Section 15G of the Securities Exchange Act of 1934. The Final Rule became effective for residential mortgaged-backed securitizations on December 24, 2015 and will become effective for all other asset classes, including non-resi ABS, CLOs and CMBS on December 24, 2016.

EU risk retention

In the European Union, similar (but far from identical) securitization risk retention rules have been in force since 2011. The EU risk retention rules apply to originators, sponsors and original lenders involved in securitizations and certain regulated investors purchasing securitization products. The EU risk retention rules apply to any securitization which is sold into Europe, regardless of the location of the assets or sponsor entity.

Dechert lawyers have extensive experience and expertise in advising sponsors and collateral managers of securitizations which wish to market to European investors. We have structured several innovative risk retention solutions for our clients, including the second European 2.0 CLO and the first European CLO to use an originator (rather than a sponsor) retention option.

Purpose of the Final Rule

The purported intention of the Final Rule was to better align the interests of securitizers with those of investors in securitizations. This will be accomplished by requiring sponsors in asset-backed securitization transactions to hold a minimum of 5% of the outstanding principal balance of each class of securities issued or by way of a vertical slice, 5% of the fair value of the securities issued by way of a horizontal slice, or a combination of the two.

Who are the risk retention parties and how to comply?

The Risk Retention Rules are complex and the manner in which risk retention can be satisfied is far from certain. The Final Rule requires the “securitizer" and its majority owned affiliates to be the risk retention party. Exactly who that is across all the various asset classes is not clear.

In the CLO space, it is the collateral manager (or its majority-owned affiliate) that will be required to hold risk retention.

For CMBS, it might be the deal sponsor or, in certain circumstances, more than 20% loan originators or the B-piece buyer.

At this point, we do not anticipate any further formal guidance from the agencies prior to the Final Rule's last effective dates. How to comply with the new rule is an even more complex question than who is required to comply. There are many outstanding questions about the modes and methods of compliance, use of affiliates, leverage, hedging and the like.

What’s next?

For the RMBS and CLO market place, risk retention is effectively here now, as risk retention structures are being put in place for deals closing in 2015. For CMBS and non-resi ABS, the industry is also beginning to respond. While the effective date for CMBS may seem a long way away, given the timelines required to structure and implement risk retention strategies, industry participants should be aware that it is imprudent to delay dealing with the Final Rule and that strategic decisions on how to effectuate compliance with the Final Rule need to be made in the near term.

Dechert is helping our clients understand these complex issues and we are working with our clients to develop and implement strategic structures to manage the risks and costs of this complex regulation.

Related Professionals

{kind=link}