DAMITT 2021 Report: Merger Investigation Activity Sinks More Deals

January 31, 2022

Fast facts

United States

- The number of significant U.S. merger investigations concluded in the first year of the Biden administration was in line with the average observed during the Trump administration.

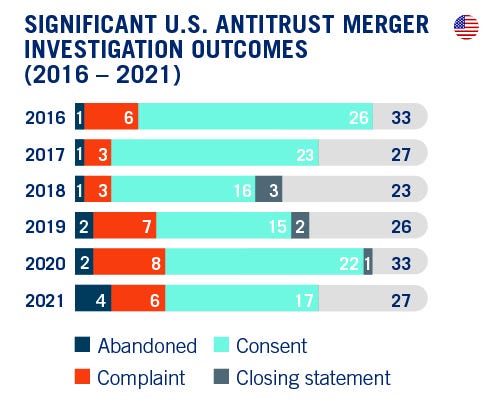

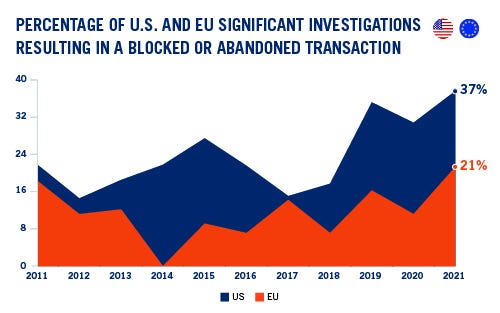

- More than 37 percent of significant investigations resulted in a complaint or an abandoned transaction, the highest observed since DAMITT launched in 2011—demonstrating increased FTC and DOJ skepticism of merger remedies.

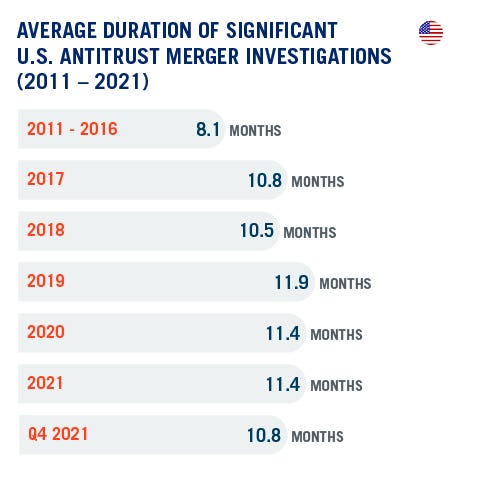

- The average duration in 2021 remained around 12 months, matching the average duration in 2020.

- We expect to see a substantial uptick in significant U.S. merger investigations concluding in 2022.

European Union

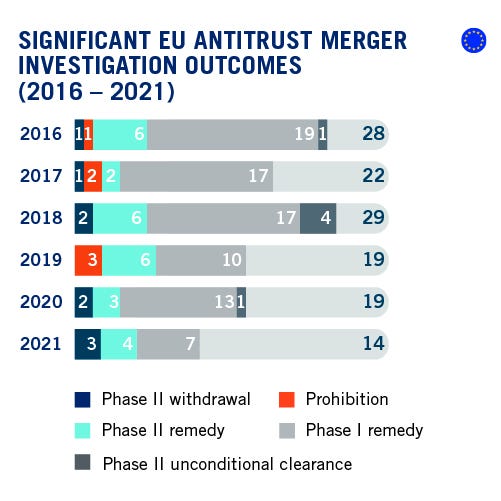

- Despite recording the second highest number of merger filings since 1990, the EU Commission concluded only 14 significant merger investigations in 2021, the fewest observed over the past 10 years.

- Twenty-one percent of these significant investigations resulted in the transaction being withdrawn or blocked, the highest ratio observed since DAMITT launched in 2011.

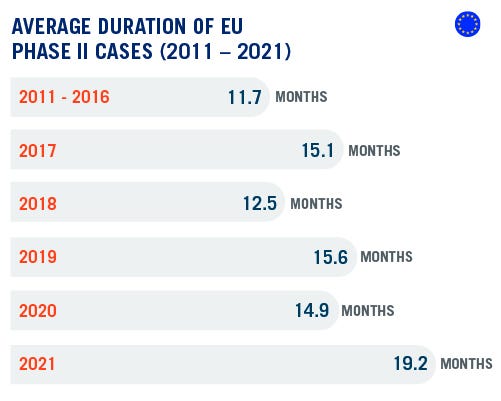

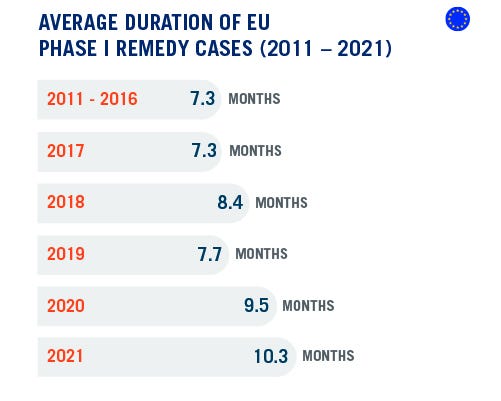

- The average duration of Phase II investigations soared 29 percent, reaching a new 19.2-month record since DAMITT started tracking. Average duration of Phase I with remedies also increased 7 percent.

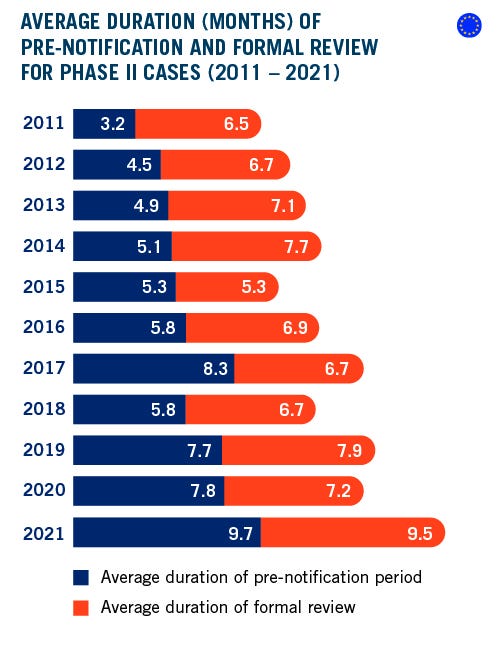

- This increased duration is due both to longer pre-filing discussions and a notable increase in the average formal review period of Phase II investigations (reaching 9.5 months for the first time) – which shows that the EC is using its stop-the-clock powers more frequently.

The Dechert Antitrust Merger Investigation Timing Tracker (DAMITT) is a quarterly study from Dechert LLP’s Antitrust/Competition practice reporting on trends in significant merger control investigations in the United States (U.S.) and European Union (EU).

In the U.S., “significant” merger investigations include Hart-Scott-Rodino (HSR) Act reportable transactions for which the result of the investigation by the Federal Trade Commission (FTC) or the Antitrust Division of the Department of Justice (DOJ) is a consent order, a complaint challenging the transaction, an official closing statement by the reviewing antitrust agency, or the abandonment of the transaction with the antitrust agency issuing a press release.

In light of the procedural differences between the EU and U.S., DAMITT defines “significant” EU merger investigations to include transactions subject to the EU Merger Regulation (EUMR) and resulting in either a Phase I remedy or the initiation of a Phase II investigation.

DAMITT calculates the durations of significant investigations in both jurisdictions from the deal announcement date through the completion of the investigation, and therefore includes the time attributable to pre-notification consultation efforts.

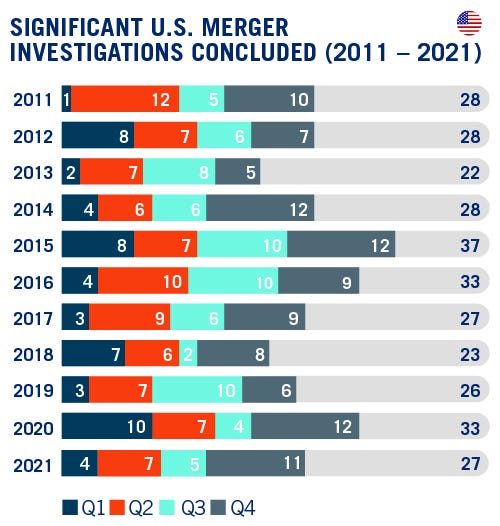

The Duration and Number of Significant U.S. Merger Investigations Concluded in 2021 Were in Line with Trump Administration Averages, But Resulted in Fewer Settlements

The U.S. antitrust agencies received 4,130 HSR filings in 2021, more than double the 1,965 recorded in 2020. Despite this flood of filings and an array of prominent policy changes from the Biden administration, the overall duration and number of significant U.S. merger investigations concluded in 2021 were consistent with the duration and number of significant investigations concluded under the Trump administration.

The 27 significant U.S. merger investigations concluded in 2021, for example, falls just below the average observed over the four years of the Trump administration. Of note, 11 of those 27 investigations concluded in Q4 2021, representing a dramatic uptick in what was otherwise a relatively quiet year for merger activity. This increase in Q4 2021 corresponds with initial reports of an elevated wave of HSR filings in Q4 2020, and it provides reason to expect an even greater increase in the number of concluded investigations in 2022.

Similarly, the 11.4-month average duration of significant U.S. merger investigations concluded in 2021 was just slightly above the average observed over the four years of the Trump administration and even identical to the average duration observed the last year of the Trump administration in 2020. The average duration of significant investigations concluding in Q4 2021 dipped slightly lower to 10.8, but there remained wide differences between individual investigations. More than half of investigations in Q4 2021 had a duration as long or longer than the 11.4-month average recorded for all of 2021.

Of note, the combined number of transactions that ended in either a complaint or an abandoned transaction in 2021 matched 2020. With fewer significant investigations concluding in 2021 than 2020, however, the 10 investigations that ended in a complaint or an abandoned transaction in 2021 represented 37 percent of all significant investigations – the highest proportion observed since DAMITT first launched in 2011. As shown below, deals abandoned without a complaint represented 40 percent of these transactions that did not result in a consent decree, the highest proportion since 2014.

These outcomes indicate that the vocal FTC and DOJ skepticism of merger remedies—which did not begin under the current administration—is in fact reducing the number of deals that end in consent decrees, highlighting the continued importance of negotiated antitrust provisions in merger agreements for transactions that proceed to significant merger investigations.

In particular, these outcomes have important implications for deal timing. The average investigation that resulted in a complaint lasted 12.7 months, slightly longer than all significant merger investigations concluding in 2021. Based on DAMITT data, parties receiving a complaint still need to plan for an additional seven to nine months from the date of the complaint to preserve their ability to litigate a transaction to a successful outcome. Parties that do not plan for that time up front may face significant timing pressure, especially given the recent FTC and DOJ announcement that they are revising the merger guidelines to strengthen enforcement against illegal mergers.

The Number of Significant EU Investigations Drops 32 Percent Below Average While Duration of Investigations Soars

2021 was a year of superlatives from an EU standpoint: the lowest number of significant investigations concluded over the past 10 years, the highest duration of Phase II investigations (with a drastic increase in the duration of formal reviews), a near record-low number of Phase I remedy investigations (but averaging a near record length); and all of this in a context of intense merger activity leading to the second highest number of EU Commission filings since 1990. Let us unpack this.

The EU Commission concluded only 14 significant investigations in 2021, half the number of significant investigations concluded in 2018 and 32 percent below the average number of investigations concluded over the past 10 years. This drop is all the more remarkable since the number of deals notified to the EU Commission was the second highest since 1990. Taking into account that the Brexit transition period expired in 2021, which was expected to decrease the EU Commission caseload by 15 percent, the high number of filings observed reflects the exceptional merger activity of 2021.

The number of Phase II investigations concluded in 2021 remains in line with previous year average, but Phase I remedy cases dropped 44 percent below the 10-year average.

Out of these 14 significant investigations, three transactions were abandoned in Phase II. Putting aside the highly political Fincantieri/Chantiers de l’Atlantique merger, the remaining deals were both airline mergers (Air Canada/Transat and IAG/Air Europa). The fact that airlines were among the first impacted by COVID-19 may have added to the already difficult assessment of routes and slot remedies typical in airlines mergers.

The pandemic also likely played a role in the extended duration of the review period for Phase II transactions. The duration of Phase II investigations concluded in 2021 set a new DAMITT-record at 19.2 months, exceeding the previous 15.6-month record set in 2019 by nearly four months. While the increase in duration is in part due to longer pre-notification periods – an increase of 26 percent compared to 2020 – another key feature of 2021 investigations is their extremely long formal review period. With an average duration of 9.5 months, the formal review of 2021 Phase II cases lasted 66 percent longer than the 10-year average. This is also more than 50 percent longer than the theoretical maximum duration of 130 working days provided in the EU merger regulation.

These longer timeframes are due to the EU Commission’s increased use of its statutory powers under the EU Merger Regulation, which allow case teams to agree to “voluntary” extensions with the merging parties and issue “stop the clock” orders. The EU Commission granted voluntary extensions in all Phase II investigations concluded in 2021. Seventy-one percent of significant investigations resolved in 2021 were suspended, for an average of three months. Time will tell whether this is a new feature of EU merger control or an effect of the worldwide pandemic. This said, with five ongoing Phase II investigations having already clocked on average 14.5 months from announcement—and the first significant decision of 2022 having been issued 36 months after announcement—we do not expect the duration of significant merger investigations to decrease in 2022. The new interpretation of Article 22 of the EU merger regulation may also push the duration of Phase II investigations up but it is too early to tell. One pending Phase II investigation that followed an Article 22 referral—Illumina/Grail —has already clocked 16.5 months from announcement; but to the contrary Meta/Kustomer, also subject to an Article 22 referral, was cleared only 14.1 months after announcement.

The duration of Phase I remedy cases also increased to a near-record duration of 10.3 months, due mainly to lengthier pre-filing talks, up nine percent compared to 2020. Pre-notification contacts are a longstanding feature of EU merger reviews: merging parties generally start pre-filing talks with the EU Commission staff very shortly after the transaction announcement, if not before. Pre-filing periods have been steadily increasing since 2016 – with the exception of 2019 – and experience shows that even in simple deals, the EU Commission requires an increasingly large amount of information before allowing a formal notification to be filed.

On the other hand, the average duration of cases reviewed under the simplified procedure remained steady at 17.6 working days. This is considerably below the maximum Phase I review period of 25 working days. Since short-form cases accounted for 78 percent of all merger investigations resolved in 2021, this is a significant counterweight to the increased duration of the review of problematic deals. The revised simplified procedure has been one of the most successful features of the 2013 overhaul of EU merger control procedures, resulting in a significant reduction in the time it takes the EU Commission to review cases that do not give rise to substantive issues. The updated notice on the simplified procedure – expected to be published in 2022 and aiming to further streamline the review process and expand the categories of deals qualifying for simplified review – may further increase the number of deals notified as short-forms in the coming years.

In the U.S. and EU, Significant Investigations Result in a Higher Proportion of Transactions Blocked or Abandoned, Even as Fewer Notified Transactions Receive Significant Investigations

As previously noted, 37 percent of all significant U.S. merger investigations concluded in 2021 ended in either a complaint or an abandoned transaction. In the EU, 21 percent of significant merger investigations similarly resulted in a prohibited or abandoned transaction. These are both DAMITT records and a notable red flag for transactions that do receive significant investigation on either side of the Atlantic. Notably, in the U.S., this follows a trend observed in the last two years of the Trump administration. The data demonstrate that the growing skepticism of merger settlements is growing in the U.S. and may also extend to the EC staff in Brussels. We do not expect this trend to reverse in 2022; indeed, the first significant investigation concluded by the EU Commission in 2022 has already resulted in a prohibition.

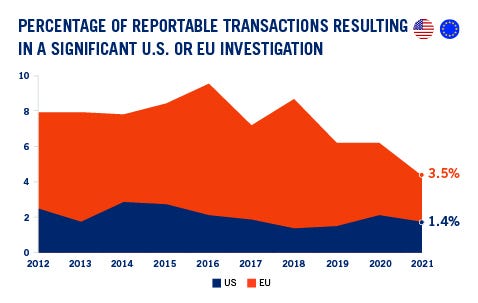

As a silver lining for parties considering transactions, however, the data also show a trend of relatively fewer notified transactions receiving significant investigations in the first place. To account for the duration of significant investigations, which can start in one calendar year and conclude in the next, DAMITT estimates the proportion of notified transactions that receive significant investigations each year by dividing the total number of significant investigations concluded each year by (i) the prior year’s number of total merger filings in the US, and (ii) the number of deals formally notified to the EU Commission in the same year. This difference is explained by the different lengths of the period between formal notification and conclusion of the average significant investigation in each jurisdiction. The results show a notable drop in the proportion of filings leading to significant investigations, especially in the EU where the proportion decreased by 4.2 points in five years.

Of note, on the U.S. side, this trend does not account for the tidal wave of merger filings that occurred in 2021. Based on this data, we would expect the number of concluded investigations to significantly increase in 2022. That said, given the overall number of merger filings in 2021, it seems likely that the percentage of filings that receive significant investigations will continue to fall in 2022 on both sides of the Atlantic.

Conclusion

Parties to transactions subject to significant merger investigations are more likely today than at any time over the last decade to see their deal blocked or to be pushed to abandon their transactions. To ensure the ability to defend their deals through a potential investigation, parties to the average “significant” deal in the U.S. should plan on at least 12 months for the agencies to investigate their transaction and may want to add on additional time to address the continuing uncertainty at the agencies. Parties should also plan for another 7-9 months if they want to preserve their right to litigate an adverse agency decision. On the EU side, parties to transactions likely to proceed to Phase II investigations should allow for at least 18 months from announcement to clearance under the current circumstances and should not rely on the theoretical deadlines provided for in the EU Merger Regulation, even after the deal has been formally notified. If the investigation is likely to be resolved in Phase I with remedies, parties should plan on around ten months from announcement to a decision.

Related Professionals

Partner

VISIT BIO

Clemens Graf York von Wartenburg

Brussels +32 2 535 5411

Munich +49 89 21 21 63 50

Subscribe to Dechert Updates